Investing for beginners, even if you don’t have a lot of money

I am amazed at how hard a time people have getting started investing. For financial independence, starting as early as possible, is the key to financial freedom further in life. If it wasn’t for me starting early, I would never be able to quit my corporate jobs and do this full time. I was also very lucky, I was always curious about markets from a young age and actually bought my first stocks with my lawn mowing money at the age of 12.

Now before you ask yourself, who the heck is this guy and why should I listen to him, let me tell you a little about me. First of all, I am not a broker, financial advisor or financial planner. But you don’t need to be to get started investing.

But before you say, Chris, what do you know about investments, hold on a second. You see, while I am not a broker, I used to be. But, I didn’t sell to people like you and me. I sold to hedge funds, insurance companies, banks and large corporate investors. And I sold fixed income securities and derivatives to these very sophisticated investors.

I also handled the banking, investments and insurance for two Fortune 500 companies, valued derivatives for huge banks and hedged foreign exchange for another one. On top of this my MBA specialties were in Finance and Financial Derivatives.

I don’t tell you this to brag, and I don’t tell you this to say, hey listen to me, I know more then you. This is also not an excuse to start talking about complicated products and financial terms. For all the sophisticated products I dealt with, my own investment philosophy is one of simplicity, low cost and low touch. I do tell you this to show you that I have some experience with investing, and even with all that experience, I keep it simple.

You might be investing already?

If you work for a company that has a 401k plan, you might be investing already. Many companies have moved to what is called negative enrollment. What this means is, unless you specifically say no, you are signed up with an initial contribution. I agree with this as investing in a 401K can have a lot of advantages.

Many companies do an initial match and if you are not taking advantage of this, you are a fool. And once you get into the upper tax brackets, maxing out your 401K doesn’t reduce your take home that much. On average I only saw a 50 cent reduction in take home for every dollar I added to my 401k.

Does your company have an Employee Stock Purchase Plan? I worked with two companies that both had Employee Stock Purchase Program. In each case, the company would bank a percentage of your salary and every six months, purchase company stock at a 15% discount to the market close. As long as there is no holding period requirement, you should be maxing this out, even if you have to borrow to do it. Worst case, you are getting a 17.5% automated return. But if you run the math properly (read the commend from Mermengil in this Reddit post https://www.reddit.com/r/personalfinance/comments/6boqgn/a_question_about_espp_and_calculating_return_a/ ) you are actually getting close to a 70% return per annum. Where else are you getting that kind of return. So yes, even if you have to fund it with credit cards you should.

Funding Retirement Accounts First

Let’s assume that you don’t have a 401k from your employer or you are self employed. If that is the case, then your first goal is to fund your own retirement programs. This means a traditional IRA, a Roth IRA or if you own your own business, a SEP IRA.

If you are in the lowest tax bracket, then you should fund a Roth IRA. But as you move up tax brackets, it makes sense to fund a traditional IRA. This allows you to fund with high marginal Pre-Tax dollars and withdraw in retirement with most likely, low Marginal Rates.

What about a SEP-IRA? If you own your own company, are a 1099 employee or freelancer, then take a look at SEP IRA. A Simplified Employee Pension IRA is one of the biggest tax give-a-ways for small business owners. In general, your “company” can fund a SEP IRA with pre-tax dollars up to 25% of income or $54,000 (which ever is less). This is more than both your traditional and Roth IRA contributions.

There are other retirement vehicles available, but these are the ones I use. Here is a simple article about other vehicles. https://www.schwab.com/resource-center/insights/content/financial-planning-self-employed

Getting Started when you don’t have a lot of money

Edit (8/3/2018): Fidelity announced today they are dropping minimum investments and minimum opening accounts to zero. That means you can start for quite a bit less than $1000. (https://www.fidelity.com/why-fidelity/pricing-fees).So now there is literally no excuse. That being said, what I write below still applies and I will still keep my account with Schwab at this time.

Ideally you need $1000 to get started. Most discount brokers will allow you to open an account with $1000. Now, a lot of you are going to say, I don’t have $500 bucks saved, let alone $1000. Fair enough, when we first start out, it can be hard. What about $100 a month? If you can afford $100 a month you can set up an automated investment plan with many online brokerages.

But yes, even $100 can scare people. So I am going to show you the trick I have used to help get many people started investing when they didn’t have a lot of excess cash. It all starts with $20 a week. You can scrounge up $20 a week. I have seen people picking out cans and coins on the ground that can find $20 a week. In fact I know some people spend double that a week at coffee shops.

With $20 a week, you can start the very first savings process. In this case, set up an account with Ally Bank. Connect your bank account, and set up an automated pull of $20 once a week. Based on current rates as I write this, by November, you will have the $1,000 you need to open an account, plus money left over in your account. What is great is even if you don’t invest, you now have $1,000 saved up as an emergency fund.

I have done this with people who have never saved in their lives and they used this to save money for a down payment. At one point I have 4 accounts pulling $50 a week into different accounts, over kill from an accounting perspective.

Where to Invest

Whether you are new to investing or experience, I recommend using Index Mutual Funds. Index Mutual funds track a basket of securities such as the S&P 500. The beauty of these are they are extremely low cost and because of this often out perform more expensive actively managed funds. And it is not just me, Warren Buffet recommends low cost index funds as well.

https://www.cnbc.com/2018/04/24/why-an-index-fund-is-warren-buffetts-favorite-way-to-invest.html

If all you have is $1000, and you have at least 10 years till retirement, go ahead and put those funds into an equity index fund, either an S&P500 Index fund or Total Stock Market Fund. I use Charles Schwab as their fees are lower than Vanguards and their technology better. Add to this, their bank account is one of the better banks accounts in the world.

Get $100 when you sign up for Schwab

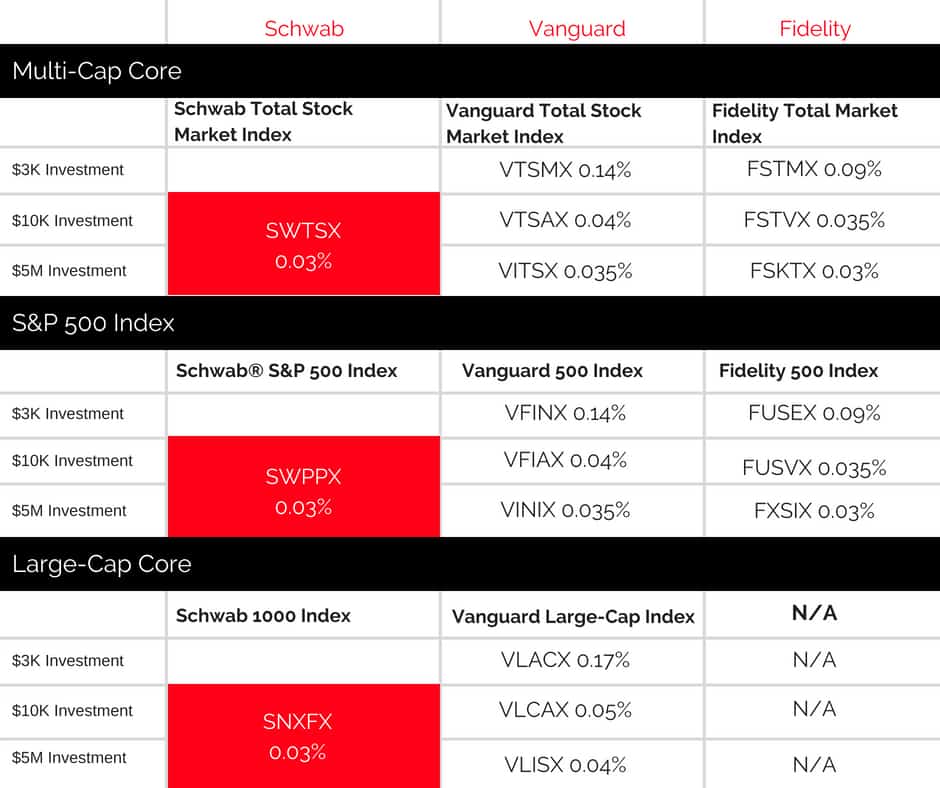

You can see in the chart below how fees compare to its competitors.

What you need to know about Fees

Most people go directly to the fund returns and make a decision from there. What most people don’t realize, is fees are taken out, after returns are calculated. So that 7% return can be reduced to 6.97% (with our Schwab Index Fund) or down to 6% with a high fee active managed fund.

I decided to run some calculations to show you the difference. Lets pretend you are able to add $1,000 a year over the next 20 years. We will also assume a 7% return. In fund A, it is the Schwab Index, that has a fee of .03%, Fund B has a fee of .5% and Fund C has a fee of 1%.

$1000 a year for 20 years

Fund A (index): $47,557.54

Fund B (.5% fee): $44,872.6

Fund C: (1% Fee): $42,199.86

You can see you give up over $5,000 just in fees from choosing the higher cost fund. Now let’s pretend you never put another dime in your account except the initial $1,000.

$1000 one time for 20 years

Fund A (Index); 3,848.04

Fund B (.5% fee): $3,523.65

Fund C: (1% Fee): $3,207.14

In this case you are giving up $600 from choosing the high fee fund. Now many people will tell you yes, but the active fund, it out performs. In most cases, it does not out perform over the long term, and for most, any out performance does not compensate for the higher fees.

Fees matter. While Vanguard is what everyone recommends, their fees are higher than Charles Schwab, and if you don’t have at least 10k, they charge you maintenance fees which is a no go for me.

Don’t I need a Financial Advisor?

You don’t need a financial advisor… yet… if ever. When you are first starting out, you do not need a financial advisor. But as you grow, your financial picture becomes more complicated, a financial advisor might become useful to you. I recommend a Fee only financial advisor that charged a flat fee. And there are actually advisors that will do one time work ups on an hourly basis for you. For those that want to do it themselves, this might be a good route to go.

You will have to ultimately make your own choice but again, I recommend using a Fee only financial advisor that accepts no other fees. These advisors usually have fiduciary responsibility to you. They do not sell product many times and will direct you either to DFA or Vanguard or if you want to stick with Schwab, go that route.

The next route would be a full service firm and yes, Charles Schwab is a full service firm. You can also look at the Robo Advisors but I don’t have an opinion on them at this time.

I avoid Insurance companies just because they will always push an insurance product.

Finally, please stay away from the MLM insurance companies like Primerica and World Financial Group.

Don’t I need Insurance

Maybe, but most likely you will not need the insurance products that an insurance sales person will try and sell you. For most of you, term life will be ideal. But if you want/need a permanent insurance solution, I would start at whole life. I would avoid any of the Universal Life Products, especially the Index Universal Life Products.

Insurance would need its very own analysis that has nothing to do with investments. That is right, on average, insurance is not an investment, its protection. Queue the insurance agents telling me how wrong I am…

Books to Read

If you want to read a little further start with the two books below and that will lead you down the rabbit hole you will not be able to get out of.

Trackbacks/Pingbacks